1 min read

ESMA’s 2025 Corporate Reporting Priorities – 5 Things You Need to Know

IFRS Financial Reporting: Strengthening Transparency The International Financial Reporting Standards (IFRS) are a globally recognized set of...

4 min read

In recent years, the audience for corporate reporting has fundamentally changed. While we still write for the human analyst, we are now equally...

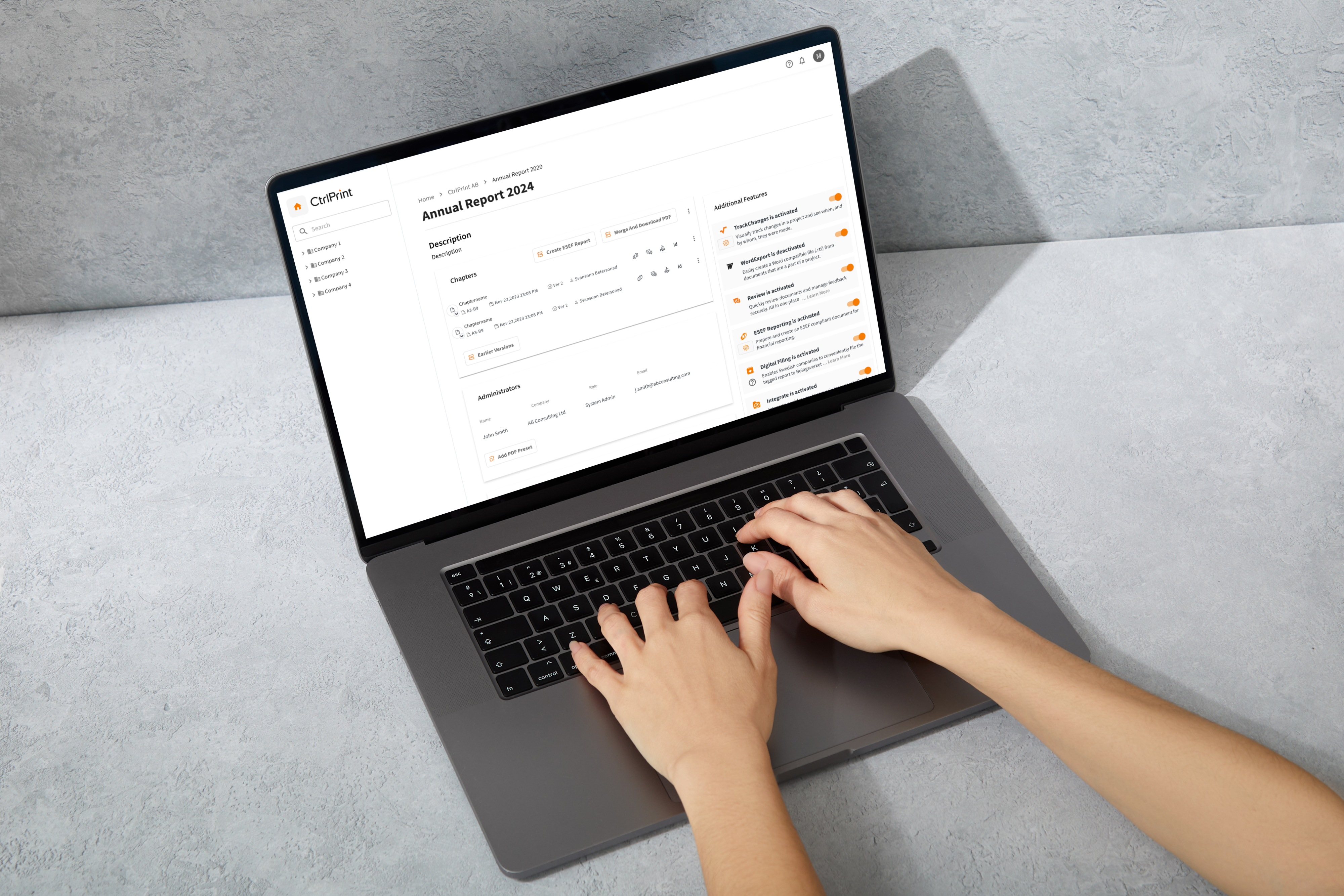

%20CtrlPrint%202026%20highlights%20and%20roadmap%20.pptx%20(1).png)

Reporting teams work under constant pressure: numbers change late, reviewers add comments across multiple chapters, and deadlines leave little room...

1 min read

IFRS Financial Reporting: Strengthening Transparency The International Financial Reporting Standards (IFRS) are a globally recognized set of...

1 min read

The EU Commission’s newly implemented Corporate Sustainability Reporting Directive (CSRD) has changed the ESG reporting way. The new framework is...

1 min read

For executives, the challenge is clear: which tools offer the automation, compliance, and collaboration needed to keep pace? With a growing market of...