AI enhanced corporate reporting whitepaper

In recent years, the audience for corporate reporting has fundamentally changed. While we still write for the human analyst, we are now equally...

5 min read

ESEF (European Single Electronic Format) is the mandatory electronic reporting format for annual financial reports published by issuers whose securities are admitted to trading on EU regulated markets.

Under ESEF, the annual financial report is prepared in XHTML (readable in a standard web browser). Where an issuer prepares consolidated financial statements under IFRS, those statements must also be marked up using Inline XBRL (iXBRL), which makes the information machine‑readable for automated analysis and comparison.

This article explains the main components of ESEF—XHTML, iXBRL tagging, and the ESEF taxonomy—and summarizes what typically changes for preparers, reviewers and auditors during the reporting process.

Looking for practical support? CtrlPrint provides tools and services for preparing and validating ESEF/iXBRL reports

ESEF introduces a common digital format intended to improve the transparency, accessibility, and comparability of annual financial reports.

At a high level, ESEF reporting typically involves:

Preparing the annual financial report in XHTML.

Marking up (tagging) IFRS consolidated financial statements in that report using iXBRL.

Using the ESEF taxonomy (an ESMA package based on the IFRS taxonomy) and creating issuer-specific extensions when needed.

Validating the ESEF package (technical, calculation and taxonomy conformance checks) before submission.

Submitting the ESEF package according to the national filing mechanism and regulator requirements in the issuer’s home member state.

In many jurisdictions, issuers also involve their auditors or another independent reviewer to perform procedures on the ESEF package, in line with local requirements and engagement scope.

The ESEF mandate is defined in EU rules and ESMA’s Regulatory Technical Standards (RTS). It requires annual financial reports to be published in a standard electronic format so that investors and regulators can access, compare and analyse information more efficiently.

What is ESEF Tagging?

Is there a difference between detailed

tagging and block tagging?

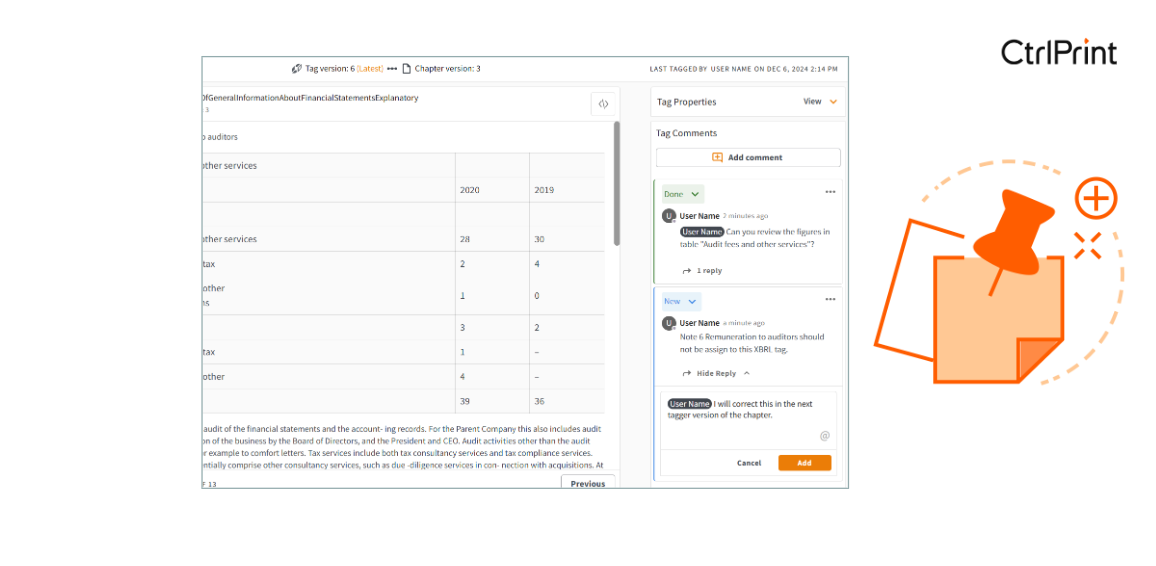

ESEF tagging is the process of applying iXBRL tags from the ESEF taxonomy to the IFRS consolidated financial statements contained in the annual financial report.

In practice, tagging is commonly discussed in two layers:

Detailed tagging of the primary financial statements (e.g., statement of financial position, profit or loss and other comprehensive income, cash flows and changes in equity).

Block tagging of the notes (tagging disclosures at section level rather than tagging every individual value).

Block tagging means assigning a single iXBRL tag to an entire disclosure section (for example, a note, accounting policy or table). The tagged block can include text, numbers and tables.

For financial years beginning on or after 1 January 2022, ESEF requires block tagging of note disclosures that correspond to the mandatory elements in the RTS annexes. The exact scope and how it is applied should be checked against the current RTS, ESMA reporting manual and any local filing guidance.

The ESEF taxonomy is the set of reporting concepts (elements), labels and technical rules used for iXBRL tagging under ESEF. It is published by ESMA and is based on the IFRS taxonomy, with additional ESEF-specific components and entry points.

Using a common taxonomy supports consistent tagging and improves the comparability of IFRS consolidated financial statements across issuers. When a required disclosure cannot be represented with an existing taxonomy element, issuers create an extension element and anchor it appropriately within the taxonomy structure (in line with the RTS).

Taxonomy packages include label resources and are distributed with entry points intended for use across EU/EEA markets; the labels and language handling depend on the taxonomy release and the tooling used.

ESEF applies to issuers whose securities are admitted to trading on EU regulated markets and who publish annual financial reports under the Transparency Directive framework. The RTS applies to annual financial reports for financial years beginning on or after 1 January 2020.

It is mandatory primarily because it supports:

better accessibility (XHTML for human readability and iXBRL for machine-readable extraction);

improved comparability (standardised tags support analysis across issuers and periods);

more efficient supervision (regulators can run structured checks and analytics on tagged data).

Non-compliance can lead to filing rejections, remediation requests or other consequences depending on local rules. For that reason, issuers typically treat ESEF as a controlled process with defined responsibilities, review steps and validation.

To turn the requirements above into a practical plan, use the checklist below as a quick way to confirm that your annual report and iXBRL tagging are ready for filing.

Use this checklist as a practical starting point for an ESEF filing. Always confirm the final requirements with ESMA materials and the filing rules in your home member state.

Confirm your in-scope reporting: ESEF applies to annual financial reports; iXBRL tagging applies to IFRS consolidated financial statements.

Confirm which ESEF taxonomy version is applicable for your financial year and local filing (taxonomy updates can become effective for new financial-year start dates).

Plan the tagging approach early, including extensions and anchoring, and align it with your reporting calendar and review capacity.

Convert the annual financial report to XHTML and ensure the visual rendering matches the approved report (layout, pagination, links and references).

Apply iXBRL tags to the primary financial statements (detailed tags) and to the notes (block tags) in line with the RTS scope.

Run technical validation (XHTML, iXBRL, taxonomy conformance, calculations) and resolve errors and warnings in a documented way.

Perform a quality review of tagging (consistency, correct signs/periods, dimensional use, anchoring of extensions, and readability of the rendered XHTML).

Coordinate any auditor/reviewer procedures early to avoid late-cycle rework.

Submit via the appropriate national filing mechanism and retain the final package, validation evidence and review logs for audit trail.

Many issuers still produce a PDF for communication purposes, but for ESEF filings the annual financial report must be published in XHTML (and, where applicable, iXBRL‑tagged). The key differences are summarised below:

|

Aspect |

PDF Report |

ESEF (XHTML) Report |

|---|---|---|

|

File format |

Static document format designed for reading and printing. |

XHTML file designed for browser viewing; IFRS consolidated statements are additionally tagged in iXBRL. |

|

Structured data |

No embedded structured tagging; data extraction is largely manual. |

Tagged data can be extracted and analysed automatically using XBRL tools. |

|

Regulatory filling |

May be used as a communication format, but on its own does not meet ESEF filing requirements. |

Designed to meet ESEF filing requirements and support regulator and market analysis workflows. |

ESEF adds a structured-data layer to the annual reporting process. For preparers, the main change is that reporting now involves both (1) producing the report in XHTML and (2) applying and reviewing iXBRL tags.

This typically requires:

understanding the taxonomy and how it maps to IFRS disclosures;

setting up a controlled tagging process (roles, reviews and documentation);

building capability to resolve validation issues and maintain consistent tagging year over year.

With the right process and tooling, much of the work becomes repeatable year over year, and teams can focus more on analysis and narrative quality rather than manual reformatting.

Auditor involvement depends on local regulation and the agreed engagement scope. Where procedures are performed on the ESEF package, auditors commonly assess whether the XHTML/iXBRL package is prepared in accordance with applicable ESEF requirements and whether the tagging is consistent with the underlying IFRS consolidated financial statements.

This can include reviewing validation results, checking selected tags and calculations, and assessing extensions and anchoring. Early coordination between the issuer, the reporting team, and the auditor helps avoid late-cycle rework.

ESEF is now an established part of annual reporting for many EU‑regulated issuers. A high-quality ESEF filing combines compliant technical packaging (XHTML + iXBRL) with disciplined tagging and review—so that the report remains readable to humans while also usable as structured data.

Because ESMA guidance and taxonomy releases evolve, issuers should monitor updates each year and keep an audit trail of taxonomy selection, tagging decisions, validation and reviews. If you would like support with ESEF preparation, validation, or process design, CtrlPrint can help.

In recent years, the audience for corporate reporting has fundamentally changed. While we still write for the human analyst, we are now equally...

%20CtrlPrint%202026%20highlights%20and%20roadmap%20.pptx%20(1).png)

Reporting teams work under constant pressure: numbers change late, reviewers add comments across multiple chapters, and deadlines leave little room...

The modern corporate reporting landscape is becoming significantly more demanding as organizations face new regulations, tighter deadlines, and...

1 min read

ESMA has released the updated ESEF Reporting Manual for year 2025 reporting. The latest edition introduces a few clarifications and tighter...

1 min read

In this article, we will cover everything listed companies in the UK need to know about UKSEF, including who is required to follow this format, the...

1 min read

[wistia_video_code id='z1atn9t1hd' title='Webinar recording'] Learnings from the recent season Join us as we dive into ESEF and conducting a...